Energy futures: A new equilibrium model for resource extraction and investment decisions

Increasingly sophisticated technologies developed in the current century to extract natural resources from costlier fields have changed the current and expected futures prices of resources, with important consequences for energy self-sufficiency and economic growth stability. In a recent paper, Alexander David, Professor of Finance at the Haskayne School of Business, University of Calgary in Canada, develops a new model that not only includes drilling and storage decisions – as in standard models – but also considers the process of exploration and development (E&D) capital accumulation, demonstrating a strong link between the slope of the energy futures curve and E&D investment.

Data from the past 30 years demonstrate some significant trends in the oil futures market. A futures contract is an agreement between a short party (typically an oil-producing firm) and a long party (typically a financial player) to exchange a set amount of oil at a specific price on a set date. In market terminology, the futures basis is the difference between the futures market price of oil and the current spot market price. The investment decisions made by oil firms have a positive relationship with the basis on oil futures contracts. At the same time, increasing investment by oil firms has led to decreasing returns for buyers of oil futures contracts.

Prof Alexander David, the David E. Mitchell Professor of Finance at the Haskayne School of Business, University of Calgary in Canada, has built an equilibrium model, which is a model to describe the economy by aggregating the behaviour of individuals and oil firms. Prof David’s model analyses the trends seen in the oil market by examining the impact of resource extraction through drilling, the effects of the amount of the commodity that the firms store, and the firms’ investment in exploration and development on current and future prices. In his paper “Exploration Activity, Long-run Decisions, and the Risk Premium in Energy Futures”, Prof David asks how oil futures prices affect exploration decisions.

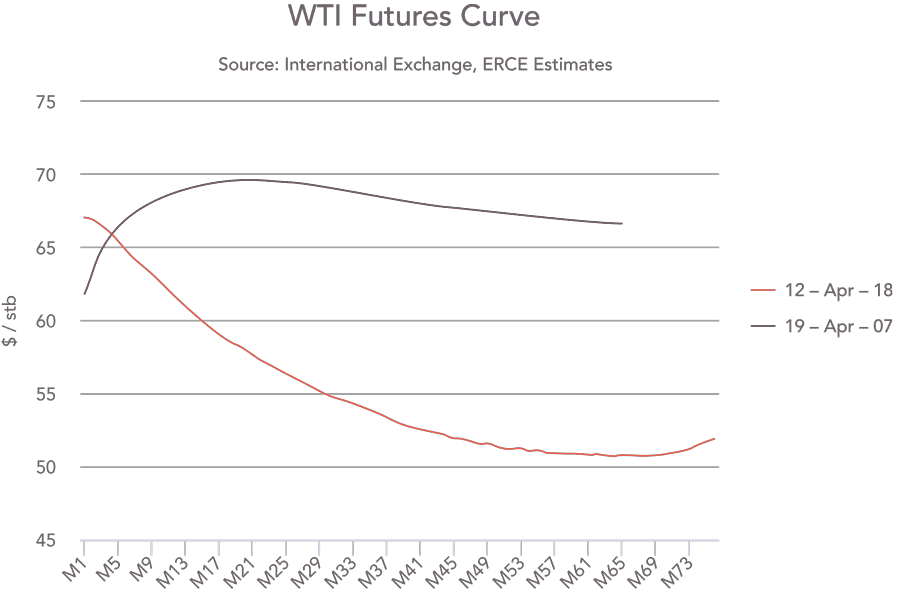

Energy futures curve

Prof David’s equilibrium model considers the short- and long-term decisions made by oil producers. His model assumes finite total reserves, with the possibility of economically accessing more resources through increased investment in machinery and other technologies. The model replicates the emerging trend of increasing costs of extracting the oil. Investment in exploration and development (E&D), and oil extraction technologies mitigate this effect to a degree.

Prof David notes that since 2000, the forward price of oil futures has been higher than the spot price (‘positive basis’), a situation known as contango, in two-thirds of the quarters. Before 2000, the forward prices of futures were lower than their spot prices (this is referred to as backwardation) in two-thirds of the quarters.

The steeper the slope is, the more attractive firms will find investment decisions or accumulating more inventory. Holding inventory is a short-term decision, whereas accumulating capital is a longer-term decision. However, Prof David shows that these two decisions are linked.

The data analysis shows that inventory decisions are the sidelight, and the main force driving the oil futures basis and the risk-premium is the E&D investment decision by oil firms.

Prof David cites the example of a situation where a firm has high accumulated capital at a point of time, the futures basis is very positive, and it experiences moderate current demand. The high capital stock makes current resource extraction efficient, and with moderate demand, making further investment would not be optimal; therefore, the firm will increase the rate of oil extraction and carry more inventory. On the other hand, if capital is currently low, so that current extraction is inefficient, then the firm would invest more currently, so that it could lower the costs of future extraction. The model accurately predicts the actual trends in the past 30 years of data.

Model developments

The two-period model starts with a linear demand function and formulas for extraction options, optimal investment, extraction, and inventory policies. The modelling clearly shows how the level of investment directly impacts the futures basis and the futures’ risk premium because it dictates the future supply of oil. A risk premium is the return that the item would make above that of a risk-free investment. After periods of strong investment, energy firms can rapidly increase oil production in response to sudden increases in demand, so that prices increase only moderately. This implies lower anticipated fluctuations in future oil prices during phases of strong investment, so that buyers of futures contracts do not need a large risk premium to take the long side of such contracts. In contrast, during phases of low investment, buyers of futures contracts must be promised a large risk premium in order to induce them to purchase these contracts.

ahorizon/Shutterstock.com

As an example, Prof David points out that in the 1990s, investment in new oil wells and technology was very limited. Subsequently in the early 2000s, there was a rapid increase in oil demand emanating from the rise of China as an economic power. With the lack of investment in previous years, oil firms were not able to increase production at short notice, and hence, oil prices increased rapidly, topping $100 a barrel. Prof David argues that astute traders in futures had already foreseen potential large fluctuations in the 1990s as evidenced by the large risk-premiums priced into futures contracts. Following the spike in oil prices, investment in new technologies such as shale drilling emerged in the mid to late 2000s. With a potentially large increase in future supply, risk premiums in the oil futures markets rapidly dropped.

Academic models for oil futures markets constructed in the past 100 years have been pre-occupied with the effects of oil inventories on the futures basis and risk premium. Even now, the financial press tracks every movement in oil inventories to shed light on the developments in the oil futures markets. However, the data analysis in Prof David’s paper shows that inventory decisions are the sidelight, and the main force driving the oil futures basis and the risk-premium is the E&D investment decision by oil firms. He hopes that his paper will lead to a change in focus of financial news reporters.

The infinite horizon model

Prof David then develops his model further to create an ‘infinite horizon model’ with three additional features in comparison to the two-period model. Firstly, inspired by Anderson, Kellogg and Salant (2018), he adds a distinction between drilling in new locations and the resource extraction from existing sites, which continues for potentially several years, albeit at a predictably declining rate. Indeed, the oil futures basis and risk premium have no relation with the total production from all existing wells (as predicted by the classic Hotelling model), but do seem to be related to the decisions by firms in the new drilling of wells.

Prof David models sudden changes in demand, known as demand shocks, such as economic downturns, which cause fluctuations in oil prices. His model considers the declining quality of resources and the decisions the energy firms are making about the amount of capital that they accumulate, given the increasing costs of extracting oil from more expensive locations.

The extraction of oil from existing wells declines over time, due to declining well pressure. However, when the model shows a demand for oil that is in line with the production of oil, the difference between the futures’ basis and the risk premium is fully explained by three factors: the activity related to drilling, the firm’s investment decisions, and the level of inventory the firm is holding.

When the capital stock is low, the cost of extracting oil is high. Prof David looks at the impact that this has upon supply elasticity. As the supply in this scenario changes at a lower percentage than the corresponding change in price, known as inelastic supply, there will only be a slight increase in extraction and a related decrease in price. There is, therefore, a strong positive correlation between future spot prices and demand shocks.

When capital levels are higher, extraction costs are low and supply increases by more than the change in the price, which is known as elastic supply. In the case of a higher demand shock, production can quickly increase, and the spot price decreases. There is, therefore, a lower correlation between demand shocks and current market prices.

As a second feature, Prof David assumes in his ‘infinite horizon model’ a habitual demand for oil consumption that equals the production from all the previous wells. Prof David argues that since wells produce at predictable rates for several years (or even decades), the energy infrastructure (for transportation as well as heating and cooling) is built with a plan to consume this future production. Since the production from existing wells is already built into plans for future consumption, the futures basis and the risk premium are only impacted by the decisions to increase or decrease drilling.

Thirdly, Prof David assumes that there are costs related to changes in investment, which are known as adjustment costs. This assumption reduces the volatility of the ratio of investment to capital that we see in the data.

How long will oil reserves last?

Prof David’s model enables us to estimate for how long we will enjoy oil supplies. The more oil that is extracted, the lower the quality of the remaining wells. In order to continue to extract oil profitably, firms must increase their level of investment in exploration and production.

Prof David estimates that the expected time for extraction to stop is in 120 years.

There comes a critical point where the amount of investment required to extract the oil becomes higher than its value, and extraction ceases even though there are natural resources still available. With simulations from his model, Prof David estimates that the expected time for extraction to stop is in 120 years. However, because the incidence of demand shocks is random, there is a reasonable chance that extraction could continue at a declining rate for another 250 to 300 years.

Over time, as the cost of extracting the oil rises, the amount of oil extracted becomes more sensitive to demand levels. Extraction would likely stop if demand fell to a low level and recommence as demand increases. Prof David’s model accurately predicts the trend we are seeing in the developed world: a dropping share of oil consumption against the consumption of goods and services.

Implications of investment

Prof David’s equilibrium model demonstrates that the level of E&D investment impacts its futures risk premium. His infinite horizon model then distinguishes between current production: resource extraction at existing sites has no effect on the risk premium while there can be observed a significant relation between the risk premium and drilling decisions at new locations. On the whole, investment decisions are the best variable for understanding the futures basis and risk premium, while inventory and resource extraction at existing sites are a sidelight. The infinite horizon model further shows that periods of very high investment can lead to a negative risk premium – meaning that return on the buyer’s investment is less than the risk-free rate. In such periods, traders price in the possibility of future oversupply of oil so that prices can decrease after an increase in demand.

Through his studies on demand shocks, Prof David also investigates the corresponding sensitivity of oil price changes. His econometric modelling demonstrates that increasing investment levels reduce the sensitivity of oil prices to demand shocks. Therefore, investment enables firms to increase their extraction and supply of oil in line with increased demand levels, so that price levels do not rise quickly.

Prof David has made a signification contribution to the existing literature through this model, and investment levels clearly remain the most important factor for understanding risk premiums and the futures basis.

Personal Response

What do you consider to be the next phase of this research?