Taming the oil price

For the foreseeable future, the world will need oil, but its price volatility makes buying and selling it a challenge for producers and the myriad manufacturers who need it. For brokers who sit in the middle of such transactions, finding the optimal price and the number of clients to spread their risk is one of their biggest challenges. Belleh Fontem, a senior researcher in operations and information systems at the University of Massachusetts, USA, has designed a mathematical programme that embraces oil price volatility. The results could have far-reaching consequences.

One of the main benefits of a highly networked global economy is the sheer scale of access to products and services. On the flip side, being so interwoven, that network is at the mercy of impactful events anywhere within it. Witness the effects when the Ever Given, one of the world’s biggest container ships, blocked the Suez Canal in March 2021, impeding the more than 1.5 million barrels of oil a day that pass through the canal. Such extreme events haunt commodity traders and risk-management executives, but it is the constant unpredictable external factors such as climate change, interest rates, and other supply-chain disruptions that they must deal with daily. Some relish the cut and thrust of such volatility, but for those who are more risk-sensitive, any tool that could help limit exposure holds much value. One senior researcher in information systems may have developed such a tool.

Belleh Fontem is an assistant professor of operations and information systems at the Manning School of Business at the University of Massachusetts, Lowell, USA. Fontem is passionate about machine learning, applied optimisation, and operations management. And mathematics. As such, finding a more effective way to manage the complexities of commodity training is both a challenge and an area worthy of his inquisitorial, scholastic eye. It is also an area of research that could settle the nerves of any risk-management executive with an eye on the company’s bottom line.

The allure of the option contract

Because commodities such as oil are traded openly on stock markets, their prices continually fluctuate. Whereas this may charge the souls of traders, it provides a significant headache for those buying and selling the real stuff. As a result, buyers and sellers usually enter into contracts, hedging their bets on whether the price will go up or down. Sellers prefer a high price, buyers one as low as possible. A successful risk-management executive, especially one in a company that relies on convoluted supply networks, who correctly ‘reads’ that price will therefore benefit their company’s bottom line. A failure to hedge accurately will place that company at the mercy of commodity spot-price uncertainty.

The programme appears a dizzying array of mathematical notation, but in essence, it embraces the very volatility of the oil price.

From a financial perspective, there are two main instruments for hedging against such uncertainty: forward contracts and option contracts. A forward contract is a tailored private contract between two parties that obliges the holder to buy/sell an agreed quantity of a commodity for some pre-specified unit price at an agreed future date. An option contract, on the other hand, involves no such obligation. Instead, it endows the contract-holding party the right, without the obligation, to buy/sell each unit of the commodity at some pre-specified maximum (or, respectively, minimum) price either until a designated maturity date or upon the realisation of a specified event. That ‘specified event’ bit increases the risk, and because there’s a greater degree of ‘room to manoeuvre’ in the contract, an underwriter plays a crucial role in ‘insuring’ the contract, betting on when the contract holder will ‘cash in’. The challenge for the underwriter, or broker, is to limit their own risk exposure by negotiating contracts with other parties willing to take opposite positions to what they hold.

For Fontem, this heightened risk made the option contract an exciting focus for research. His theory: was it possible to refine the design of an option contract to make it more attractive to risk-sensitive buyers of a critical product cursed with high price volatility, therefore increasing the number of potential clients for a broker? His tools of the trade: mathematics and a particular interest in developing computationally efficient techniques for highly complex business situations.

Seemingly counterintuitive

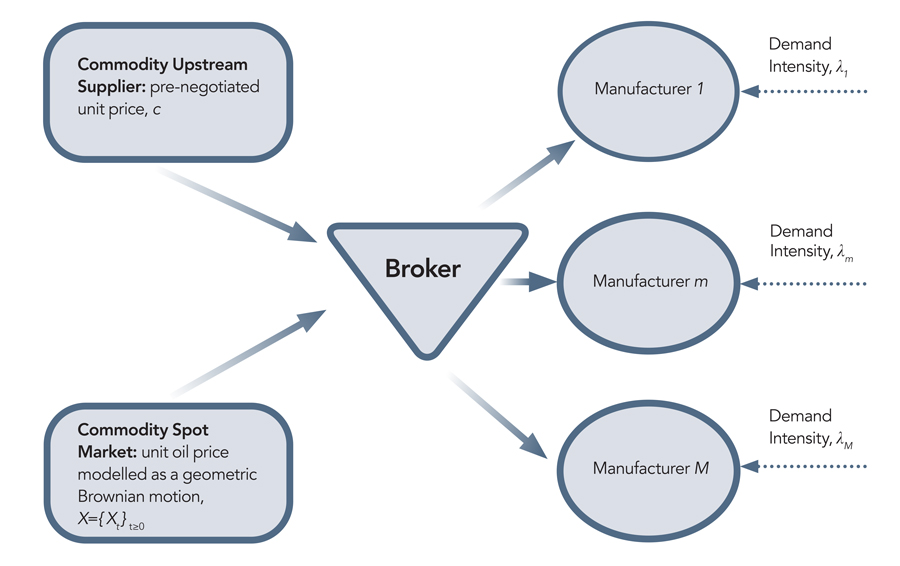

Fontem’s focus was a risk-sensitive oil brokerage firm in the southern US that sits in the middle of a two-echelon supply chain – upstream is an oil company that supplies oil, and downstream various manufacturers of products such as plastics and fertilisers, that buy the oil. The brokerage firm has two challenges. The first is calculating the unit oil cost-ceiling of the option contract suitable for the seller and buyers. This is the ‘trigger’ price that defines the option contract. The second is constructing the optimal set of clients the brokerage need to agree to such a contract to maximise the payoff per unit demand. The two challenges are co-dependent, and the firm can’t have one without the other.

Using differential calculus, geometric Brownian motion and numerical experimentation, Fontem modelled the broker’s dilemma as a mixed-integer non-linear programme that considered the complexities driving oil price volatility and reformulated it into a single-level univariate problem. For those without an advanced understanding of mathematics, the programme appears to be a dizzying array of mathematical notation, but in essence, it embraces the very volatility of the oil price to produce both the optimal structure of the broker’s option contract and their optimal set of manufacturing clients.

Furthermore, the programme unearthed some interesting, seemingly counterintuitive, insights, not least that the option contract’s optimal value increases with the commodity’s spot market volatility and decreases with its drift, or growth rate.

This realisation was important because, at its heart, an option contract for the broker’s manufacturing clients is supposed to mitigate the risks of the price volatility of a critical component of their products. Therefore, any contract that embraces volatility is optimal and highly attractive to potential buyers – a major win for the broker. But there’s an added benefit: for the supplier, any contract that is attractive to buyers increases the number of potential buyers and is therefore attractive to them as well. The result is a win–win.

Belleh Fontem has designed a mathematical programme that embraces oil price volatility. The result could have far-reaching consequences.

Calming the stormy price

Fontem’s work has significant potential impact. Not only could it rewrite option contract design for individual brokers and their clients, but it could contribute to overall better risk management and supply-chain management. This, in turn, could contribute to less oil price uncertainty in the broader US economy and thus a greater capacity for businesses, even households, to plan over longer horizons. On an even wider scale, given the current global reliance on oil and the political and economic impacts of its supply and demand, any measure that can calm its stormy price can have far-reaching consequences.

Fontem is already looking at how he can expand the scope of his research to factor-in other complexities such as local volatility, using time as a variable. There are other avenues of exploration for further study in risk quantification and commodity brokerage, such as adapting this model to other traded commodities.

There is little chance that traders and brokers who thrive on the challenges of commodity price volatility will throw in the towel any time soon – the highly-networked global economy is still riven with uncertainties that shape supply and demand. But if the global economy is to find a firm footing and grow in a way that lifts the prospects of those living lives very different to successful commodity traders, it needs an element of stability. Therefore, it will require the insights of those finding formulas for taming price volatility. In that respect, Fontem’s research into client selection and contract design for a risk-averse commodity broker in a two-echelon supply chain will play a key role.

Personal Response

Where do you see a logical extension of your work by other researchers in your field?

One way to extend our work would be to model the spot price of oil using a more sophisticated mathematical framework than geometric Brownian motion. For instance, a jump-diffusion model can more accurately handle the complications arising from sudden shocks in the price of oil. Another extension would be to quantify the broker’s payoff risk using measures other than variance. Examples would be value-at-risk, or conditional value-at-risk, which are popular risk measures in the discipline of financial risk management.